Weak internal controls are responsible for almost half of all fraud, according to the Association of Certified Fraud Examiners (ACFE).

So how do you ensure your system isn't making your organization an easy target for fraud? Use a model designed by experts to design and implement your internal controls. One of the most commonly-used frameworks was written by the Committee of Sponsoring Organizations of the Treadway Commission (COSO).

This simple guide to the COSO framework outlines how you can use it to develop a strong, effective internal control system.

Don’t gamble with your company’s investigation processes.

Request your demo of Case IQ to find out how users are saving time, closing more cases, reducing risk, and improving compliance.

What is COSO? Understanding Its Founding Organizations

COSO is a committee composed of representatives from five organizations:

- American Accounting Association

- American Institute of Certified Public Accountants

- Financial Executives International

- Institute of Management Accountants

- Institute of Internal Auditors

Together, the COSO board develops guidance documents that help organizations with risk assessment, internal controls and fraud prevention. Their vision is to "be a recognized thought leader in the global marketplace on the development of guidance in the areas of risk and control which enable good organizational governance and reduction of fraud."

RELATED: Corporate Fraud Prevention: The Ultimate Guide

Evolution of the COSO Framework and Its Core Principles+

The original COSO framework was developed in 1992, with the most recent version published in 2013. To understand the framework, you must understand what it covers. According to COSO, internal control:

- Focuses on achieving objectives in operations, reporting and/or compliance

- Is an ongoing process

- Depends on people's actions, not merely written policies and procedures

- Provides assurance senior management of security to a reasonable degree

- Can be adapted to the needs of the whole organization as well as each department, unit or process

The 3 Key Objectives of the COSO Framework

The COSO framework divides internal control objectives into three categories: operations, reporting and compliance.

Operations objectives, such as performance goals and securing the organization's assets against fraud, focus on the effectiveness and efficiency of your business operations.

Reporting objectives, including both internal and external financial reporting as well as non-financial reporting, relate to transparency, timeliness and reliability of the organization's reporting habits.

Compliance objectives are internal control goals based around adhering to laws and regulations that the organization must comply with.

The Five Key Components of the COSO Framework

The COSO framework further teaches that there are five components to an internal control system. First, control environment is the "set of standards, processes, and structures that provide the basis for carrying out internal controls across the organization." This component includes your:

- Ethical values

- Organizational structure

- Commitment to employing competent employees

- Human resources policies

Next, risk assessment involves your organization's analysis of the risks posed by internal and external changes, the ability to establish objectives and determine their suitability for your business and the process for weighing risks versus risk tolerances.

Control activities are the tasks and activities (laid out by organizational policies and procedures) that help you achieve your internal control objectives. These include actions such as "authorizations and approvals, verifications, reconciliations, and business performance reviews."

The information and communication component recognizes these two things as essential to any internal control system. COSO stresses the importance of relevant and high-quality information to control functions. Internal messages emphasizing the importance of control responsibilities, in addition to clear communication of expectations with external parties, is key to a strong system.

Finally, monitoring your internal controls is just as important as establishing them. Use ongoing evaluations built into your business processes as well as regular separate evaluations, which will vary based on your level of risk, system effectiveness and regulation requirements.

Internal Control—Integrated Framework (Framework), © [2013] Committee of Sponsoring Organizations of the Treadway Commission (COSO). All rights reserved. Used with permission.

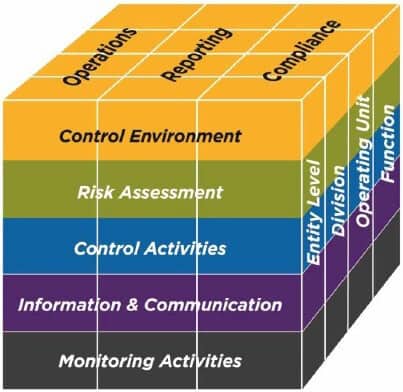

Understanding the COSO Cube: Structure and Key Principles

The image of the cube shows the relationship between all the parts of an effective internal control system.

The columns are the three objective categories (operations, reporting and compliance). The rows consist of the five components. Your organizational structure fits into the third dimension of the cube.

The framework also lists 17 principles you should apply to meet your organization's internal control objectives, divided by component.

Building an Effective Internal Control System with COSO

The COSO framework explains that "an effective system of internal control reduces, to an acceptable level, the risk of not achieving" objectives. When developing your system, make sure that:

- All five components are present and working properly

- The five components work together as an integrated system

- It allows the organization to predict external circumstances that could impair the achievement of your objectives and prepare for them appropriately

- It follows reporting regulations, rules and standards

- It complies with applicable laws, regulations, etc.

COSO recognizes that, while its framework should help you design a fraud-deterring system of internal controls, it's not without limitations. For example, even the strongest system can't prevent human error, bad judgement and external events that are beyond your control.

Find out how case management software can help you conduct more effective fraud investigations with our free eBook.

Applying the COSO Framework Across All Levels of Organization

After reading the COSO framework, senior management and other decision-makers in your organization should use it to assess your current internal control system. Does your system meet all of the effectiveness standards? If not, make plans on how to improve it according to COSO's model.

Lower-level managers and employees should also familiarize themselves with the COSO framework. Offer suggestions based on the document to senior management. Put together a committee of employees at all levels to brainstorm ideas for a stronger internal control system.

In addition, every employee should take their role in preventing fraud seriously. Conduct your work in a way that supports the COSO framework. For example, follow anti-fraud policies without exception and always file timely, accurate reports.

Benefits and Limitations of the COSO Framework

The COSO framework is a great place to start when designing or modifying a system of internal controls. However, it is not without limitations.

For instance, the framework is intentionally broad in order to apply to a wide array of industries and processes. This feature can be problematic, though, for "more complex businesses (e.g., those with varied operations and complex data systems)", according to experts from East Carolina University.

They also mention that "proper execution of the COSO framework is dependent on the ability to establish a strong, formal control environment; however, the framework provides minimal implementation guidance." Small businesses and startups may feel overwhelmed and unsupported, leading them to use a model with a more detailed framework instead.

In addition, the COSO framework is not designed well to deal with objectives that fall under multiple categories. Not every task fits neatly into either operations, reporting or compliance. Risk management expert Matthew Leitch wonders, "what about financial reporting that must be reliable to be compliant? Where do you draw the line between data processing for doing business and data processing for financial reporting?"

If you're looking to create a system of internal controls or improve upon your current one, the COSO framework is one worthy option. Read through the executive summary to see if it's a good fit for your organization.

Download our free cheat sheet for helpful tips on workplace fraud prevention.

Benefits:

1. Enhanced Internal Controls

The COSO framework’s five components help organizations build a robust internal control system. These controls minimize opportunities for errors, fraud, and mismanagement.

2. Improved Risk Management

COSO’s focus on identifying and assessing risks at all levels ensures that organizations can anticipate and address potential threats before they escalate. Proactively managing risks protects assets and enhances business continuity.

3. Increased Regulatory Compliance

By aligning with COSO principles, organizations strengthen their compliance with regulatory requirements such as Sarbanes-Oxley (SOX), reducing the likelihood of costly penalties and reputational damage.

4. Better Decision-Making

The COSO framework promotes a culture of transparency and accountability, ensuring that management has accurate, timely information to make informed decisions.

Adopting the COSO framework not only strengthens governance but also instills confidence among stakeholders, positioning organizations for long-term success.

How to Implement the COSO Framework in Your Organization

Implementing the COSO framework can enhance an organization’s internal controls, reduce risk, and ensure regulatory compliance. Follow these steps to integrate COSO principles effectively:

Step 1: Assess Your Current Internal Controls

Begin by evaluating the effectiveness of your current internal control system. Identify any gaps or weaknesses in processes related to financial reporting, operational efficiency, and compliance. Conduct internal audits and gather feedback from relevant departments to gain a clear understanding of existing control measures.

Step 2: Define Business Objectives and Risk Tolerance

Establish clear business objectives aligned with your organization’s mission. Identify potential risks that could hinder the achievement of these goals and determine your organization’s risk tolerance. Consider both financial and operational risks, ensuring that your risk assessment covers all areas of the business.

Step 3: Establish COSO’s Five Components in Daily Operations

Integrate the five COSO components into daily workflows:

- Control Environment: Foster a culture of ethics, integrity, and accountability.

- Risk Assessment: Continuously identify and analyze risks that may affect business objectives.

- Control Activities: Implement preventive and detective controls to mitigate risks.

- Information & Communication: Ensure accurate, timely, and relevant information is communicated to stakeholders.

- Monitoring: Regularly assess the performance of internal controls through ongoing evaluations.

Step 4: Monitor and Adjust Based on Audits and Performance

Conduct regular audits to assess the effectiveness of your internal controls and identify areas for improvement. Use audit findings to refine processes, address control deficiencies, and adjust risk management strategies. Establish a cycle of continuous monitoring and improvement to maintain a strong internal control environment.

By following these steps, organizations can leverage the COSO framework to enhance governance, mitigate risk, and achieve operational excellence.

COSO Framework vs. Other Internal Control Frameworks

Organizations seeking to strengthen internal controls and compliance often compare the COSO framework with other internal control frameworks, such as COBIT, ISO 31000, and the Basel Framework. Each framework offers unique approaches to managing risk and ensuring regulatory compliance.

1. COSO vs. COBIT

COBIT (Control Objectives for Information and Related Technologies) focuses primarily on IT governance and information security. It is ideal for organizations prioritizing IT risk management and cybersecurity. While COSO takes a broader approach, covering enterprise-wide internal controls, COBIT is more specialized for IT environments.

2. COSO vs. ISO 31000

ISO 31000 provides guidelines for risk management, emphasizing a risk-based approach to decision-making. Unlike COSO, which focuses on internal controls, ISO 31000 concentrates on identifying, analyzing, and managing organizational risks, making it a complementary rather than competing framework.

3. COSO vs. Basel Framework

The Basel Framework is primarily designed for financial institutions to manage operational, credit, and market risks. It includes capital adequacy standards and regulatory requirements. While COSO offers a comprehensive internal control framework, the Basel Framework is highly specialized for the banking sector.

How Organizations Choose the Right Framework for Compliance Needs

Selecting the right framework depends on industry requirements, organizational goals, and regulatory obligations. Many organizations integrate COSO with specialized frameworks like COBIT or ISO 31000 to create a tailored internal control and risk management system. COSO’s flexibility makes it a preferred choice for organizations seeking a scalable, enterprise-wide control framework.

Common Challenges in COSO Implementation and How to Overcome Them

Implementing the COSO framework can significantly strengthen an organization’s internal controls, but the process is not without challenges. Addressing these obstacles effectively ensures smoother adoption and long-term success.

Challenge 1: Resistance to Change in Organizations

The Challenge: Employees may resist changes to established processes, viewing COSO implementation as an unnecessary disruption.

Solution: Gain executive buy-in early and clearly communicate the benefits of the COSO framework. Emphasize how enhanced controls improve efficiency, reduce risk, and protect the organization. Engage employees through training and provide opportunities for feedback to foster a culture of compliance.

Challenge 2: Lack of Knowledge and Training

The Challenge: Organizations often lack the expertise needed to implement COSO effectively, leading to misinterpretations or incomplete adoption.

Solution: Invest in comprehensive training programs that educate staff at all levels about COSO principles and best practices. Consider hiring consultants or partnering with experts to guide the initial implementation process. Ongoing education ensures that employees stay informed as the framework evolves.

Challenge 3: Ensuring Integration with Existing Compliance Frameworks

The Challenge: Integrating COSO with other established compliance frameworks can be complex, leading to potential overlaps or gaps.

Solution: Conduct a thorough gap analysis to identify areas where COSO can complement existing frameworks such as ISO 31000 or COBIT. Develop a unified compliance strategy that aligns COSO with the organization’s broader governance, risk, and compliance (GRC) objectives.

The Future of Internal Controls with COSO

As business environments grow more complex, the COSO framework continues to evolve to meet modern challenges and regulatory expectations. Organizations that stay ahead of these changes can strengthen their internal controls and safeguard their operations.

How COSO Continues to Evolve with Modern Business Needs

COSO has expanded its focus beyond financial controls to include operational, technological, and environmental risks. Recent updates incorporate principles of enterprise risk management (ERM), emphasizing the need for integrated governance processes. As digital transformation accelerates, COSO is also addressing cybersecurity, data privacy, and supply chain vulnerabilities.

Why Companies Should Invest in Strong Internal Control Systems

A robust internal control system protects against financial losses, enhances regulatory compliance, and strengthens stakeholder confidence. Investing in COSO ensures that organizations can adapt to emerging risks, improve decision-making, and maintain long-term operational stability. As regulatory scrutiny increases and technological disruptions grow, companies with strong internal controls are better positioned for success in an unpredictable business landscape.

FAQs

1. What are the 5 principles of COSO?

The five principles of COSO are: (1) Control Environment, (2) Risk Assessment, (3) Control Activities, (4) Information and Communication, and (5) Monitoring Activities.

2. What are COSO requirements?

The COSO framework outlines requirements for an effective internal fraud control system, including the presence and proper functioning of all five principles, their integration into an overall system, preparation for external circumstances affecting objectives, compliance with regulations and laws, and adherence to reporting standards.

3. What is the most important component of COSO?

The most important component of COSO is the control environment, which encompasses the set of standards, processes, and structures that help detect and prevent internal fraud, including ethical corporate values, organizational structure, commitment to employing competent and ethical employees, and HR policies.

4. How can organizations implement the COSO framework effectively?

Organizations can implement the COSO Framework by assessing existing internal controls, identifying risks, aligning goals with the framework's principles, and creating actionable policies. Regular training and audits ensure continuous improvement.

5. What are examples of the COSO framework in practice?

Examples include companies improving financial reporting accuracy, enhancing risk assessment processes, or aligning compliance efforts with regulatory standards.

6. What industries benefit the most from using the COSO framework?

Industries such as finance, healthcare, manufacturing, and government benefit from improved compliance, risk management, and operational efficiency.

7. Is the COSO Framework required for all companies?

No, the COSO Framework isn’t legally required for all companies, but it’s widely adopted as a best practice for internal controls and risk management. Public companies, especially those in financial services and publicly traded firms, often use COSO’s internal control framework to comply with regulatory requirements like SOX compliance and SEC reporting standards.

8. How does the COSO Framework help prevent fraud?

The COSO Framework strengthens fraud prevention by establishing clear internal controls, risk assessments, and monitoring processes. By emphasizing ethical values, control activities, and information transparency, COSO helps organizations detect and reduce fraudulent activities before they escalate, ensuring stronger compliance and financial integrity.

9. How does the COSO Framework support risk management?

The COSO Framework provides a structured approach to identifying, assessing, and mitigating risks within an organization. It integrates risk assessment, control activities, and monitoring systems to help businesses anticipate potential threats and respond proactively. By aligning with enterprise risk management (ERM) principles, COSO enhances strategic decision-making and operational resilience.

10. What is the difference between COSO and SOX compliance?

COSO is a voluntary framework for improving internal controls and risk management, while SOX compliance is a legal requirement under the Sarbanes-Oxley Act, primarily focused on financial reporting and corporate accountability. Companies often use COSO’s internal control framework to meet SOX compliance standards, but SOX mandates strict auditing, reporting, and documentation requirements for public companies.

Resources

Internal Control—Integrated Framework (Framework), © [2013] Committee of Sponsoring Organizations of the Treadway Commission (COSO). All rights reserved. Used with permission.