#Article

How to Use AI to Improve Your Fraud Investigations

Machine learning models analyze data and spot patterns to catch fake accounts, fraudulent transactions, account takeover, promotion abuse and more.

According to the ACFE, organizations lose an average of five percent of their revenue to fraud every year. As fraudsters become more sophisticated in their schemes, investigators must keep up to keep annual losses to a minimum.

Now, with the rise in popularity of AI tools like ChatGPT, fraud investigators are wondering how they can use them to improve their investigations. Using machine learning for fraud detection and prevention makes these processes faster, less expensive and more accurate. Plus, when human analysts complement the machines by tackling new cases or complex problems, you can manage risk twice as effectively.

Free eBook

Organize your fraud data and conduct more effective investigations.

Case IQ makes it easy. Learn more in our free eBook.

Get the eBookWhat is Machine Learning?

Machine learning is, according to Microsoft, an application of AI that uses “mathematical models of data to help a computer learn without direct instruction. This enables a computer system to continue learning and improving on its own, based on experience.” In other words, a machine analyzes lots of data to “learn” about the past and predict behavior in the future.

Credit: Intellias

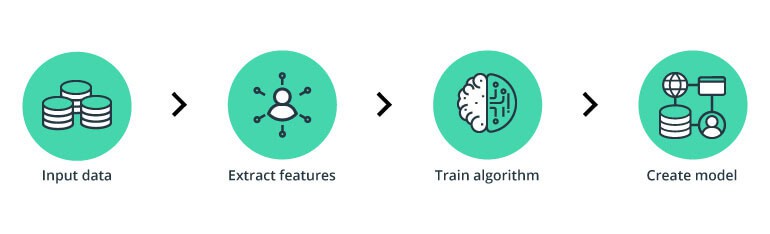

In the context of using machine learning for fraud detection and prevention, there are four steps to creating a machine learning model.

- Input data. For financial institutions, this is customer data, but for workplace fraud, you should include data from accounts payable and receivable transactions.

- Add features that describe legitimate and fraudulent behavior. Examples of features include transaction location, age of account, payment method and average transaction value.

- Launch a training algorithm to test the machine learning model. This is a set of rules, based on the input data, that the model will follow to analyze transactions.

- Update the models frequently to keep up with new fraud schemes.

RELATED: Synthetic Identity Theft: A Serious Threat for Financial Institutions

How to Use AI in Fraud Investigations

Types of Models

Machine learning for fraud detection uses one of four types of model.

Supervised learning models rely on their training algorithms to determine if transactions are legitimate or fraudulent. They can only identify behaviors that were included in their original input data.

Unsupervised learning models learn to detect patterns with little to no data about what behavior is good or bad. They continuously analyze transactions to update themselves.

Semi-supervised learning models use both data that is tagged as legitimate or fraudulent and patterns they discover on their own.

Finally, reinforcement learning models rely on reinforcement from humans to learn if they make the right decisions. A programmer either rewards or penalizes the machine based on how the model identifies a behavior. It is a trial-and-error approach to help the model learn and remember patterns.

RELATED: Phishing Spoofing and Whaling: Tips for Keeping Your Company Safe

Who Should Use AI?

Organizations in a wide variety of industries can use machine learning for fraud detection. If your company uses online accounts or receives or makes payments, you can use this technology.

Some of the most common industries that use machine learning for fraud detection include:

- FinTech

- Banking

- Online gambling and gaming

- Healthcare

- Insurance

- Ecommerce

This technology can help you spot not only fraudulent transactions, but also fake accounts, account takeovers and promotion abuse. Machine learning models can even learn to flag unpaid cash on delivery transactions.

For example, if a customer plays a prank or refuses to answer the door and doesn’t pay for their order, the model recognizes that the transaction is unpaid. It then learns patterns about who, where and what types of orders this happens for frequently, helping you prevent future incidents.

Regardless of your industry, create a machine learning model using your own data, if possible. Examples of legitimate and fraudulent behavior differ not just between industries, but even from one company to another. For instance, it would be normal for a customer to spend $1,000 in one transaction at an online furniture retailer, but probably not on a coffee shop app.

Free Checklist

Make sure your fraud investigations are timely, thorough and well-documented.

Download our fraud investigation checklist so you never miss a step.

Download the ChecklistBenefits of Machine Learning for Fraud Detection and Prevention

Vince Walden, CFE, CPA, and CEO of KonaAI, recently spoke at the ACFE Global Fraud Conference about using AI for fraud. “It is clear to see,” explains the ACFE, “that fraud examiners can benefit immediately from the use of LLMs and Generative AI. However, as fraud examiners, Vince reminds us, ‘It is your job to investigate, it is your job to validate.’ Attendees [of the session] were reminded that technology-assisted review (TAR) is a nice middle ground when implementing the use of different machine learning tools.”

Greater Work Capacity

Humans can only do so much in a day. They need breaks and time to sleep. Machine learning models, though, can work 24/7 without getting stressed out, bored or tired. Unlike human analysts, they also learn patterns and never forget them, so their effectiveness isn’t tied to memory or mood.

This not only applies to fraud, but also other applications of AI. For instance, HR professionals can use AI applications for “many tasks, from writing job descriptions to sourcing vendors to conducting market research on compensation,” according to SHRM. Small or time-strapped teams can use AI to ensure everything gets done. For instance, Carol Kiburtz, vice president of HR for Halff, at the SHRM Annual Conference said that her team is “using it to create policies, . . . employee guides and more,” she said.

Higher Efficiency

Machines can process more information at a faster rate than human analysts. This, in turn, lets you conduct the same amount of work at a much smaller cost. Not only does machine learning reduce the number of billable hours an organization has to pay its employees, but it may also reduce losses due to fraud.

Free Cheat Sheet

Want to learn more about how to use machine learning for fraud detection?

Check out our free cheat sheet.

Get the Cheat SheetMore Effective

Because they study so much data, machine learning models can discover patterns of fraudulent behavior that might go unnoticed by human analysts. Trends that are subtle, non-intuitive or seemingly unrelated to a person can easily be caught by a machine.

With new fraud schemes and an ever-growing volume of data to sort through every day, it can be hard for even the most skilled human analyst to keep up. However, machine learning models actually become more precise as they analyze more information.

Frees Up Time for Analysts

When human workers aren’t bogged down with data analysis, they have more time to handle urgent and complex cases. Machine learning helps with insights and reporting, reducing the amount of tedious work each analyst must complete. In addition, analysts can address strategic work and mistakes faster, helping your organization maintain and attract new customers.

How Case IQ Can Help

Want to conduct more effective fraud investigations? Case IQ’s modern case management software allows you to track, manage and prevent fraud and theft all in one secure platform. Our award-winning reporting tool analyzes your data and creates reports in seconds, helping you make more informed business decisions. Find out more here.